Housing affordability

OUR GOAL

All Canadians can afford a good home by 2030

Canada’s dysfunctional housing system is a painful symptom of generational unfairness, which even our federal government recognizes.

A growing number of younger people and newcomers to Canada are facing crushing unaffordability thanks to prices that rose over 300% since 2000, dragging up rent costs in their wake. These same skyrocketing prices are creating tax-free wealth for many home owners, especially older Canadians who had the good fortune to buy into the market decades ago.

No silver bullet can solve this complex problem, so we have to use silver buckshot.

Our housing policy solutions map out all the paths and principles we should follow to make homes affordable for all Canadians.

Read full details of our Housing Policy Solutions

Reaching our goal is a massive undertaking, so we're working alongside many other researchers and advocates in Canada's housing ecosystem. We support the leadership others provide to end homelessness, scale up non-market housing, and fix the regular housing market in which most Canadians find homes as owners or renters. We're currently focused on breaking Canada's addiction to high and rising home values.

REACHING OUR GOAL

Gen Squeeze is breaking our addiction to high and rising home values by pushing Canada to:

Stop counting on rising home values to drive economic growth

Governments across Canada have spent years assuming rising home prices will drive economic growth. This strategy has harmed younger people, renters and newcomers, more and more of whom are locked out of unaffordable housing markets.

To restore affordability for all, Gen Squeeze encourages Canadians and their governments to celebrate stalling home prices so that earnings can catch up. Stalling prices shouldn’t be seen as a sign of ‘weakness’ in the housing market. This attitude assumes that the primary purpose of housing is as an investment strategy to grow wealth – not a place to call home. We can no longer pursue an economic strategy that grows the major cost of living out of reach with what Canadians earn from their jobs. Stalling home prices will prioritize hard work paying off today the way it did for previous generations.

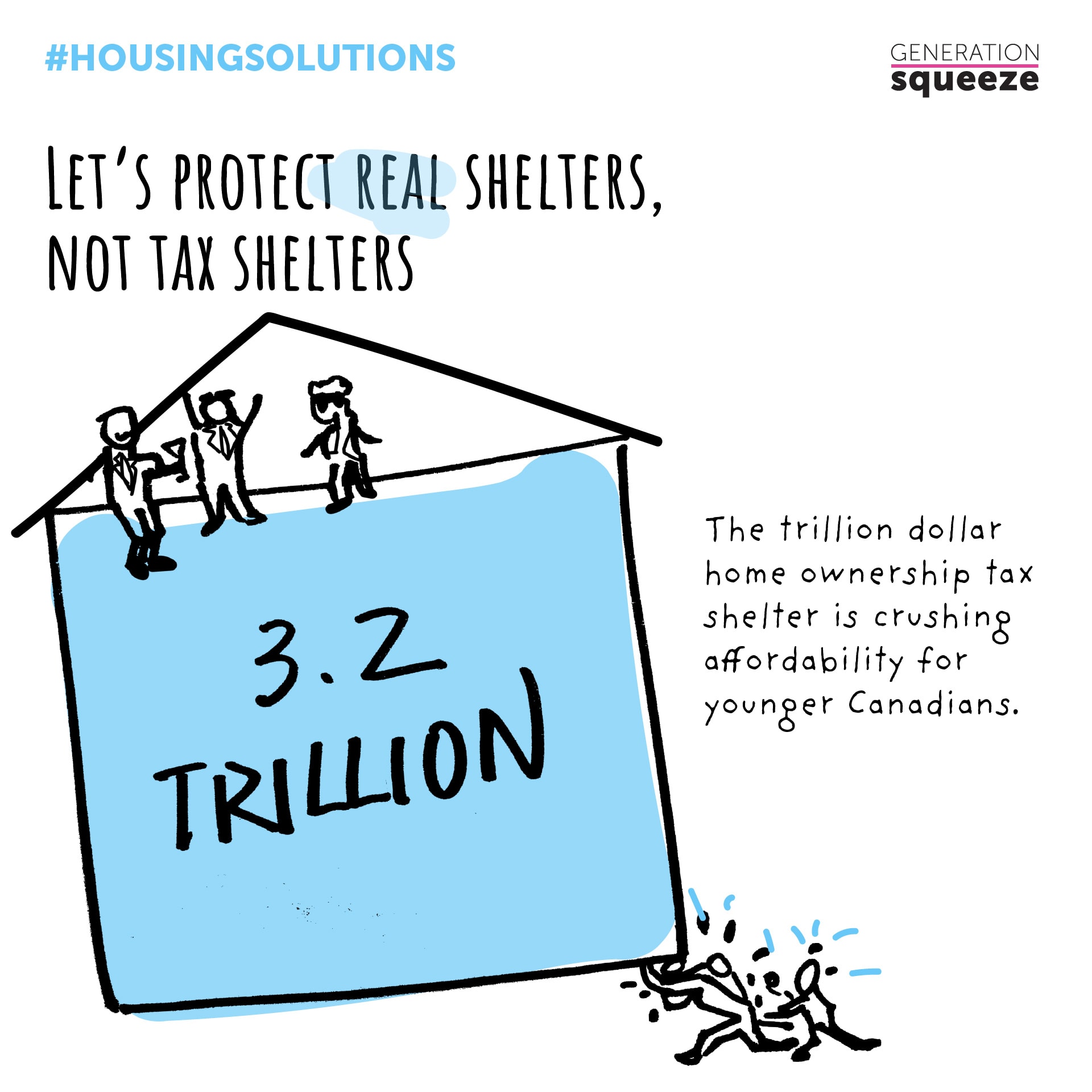

Put a price on housing inequity

Canada shelters from taxation the $3.2 trillion in housing wealth homeowners have gained since 1977. Just like offshore tax shelters motivate moving money out of Canada to preserve assets, this home ownership tax shelter motivates us to bank on rising home prices to gain wealth.

Gen Squeeze believes that it’s time to protect real shelters, not tax shelters. It’s unfair to sustain a system in which the hard work Canadians do every day in their jobs is taxed more than the wealth homeowners gain from rising prices while they sleep and watch TV.

The first step is putting a price on housing inequity by adding a modest surtax on homes valued over $1 million. This surtax will apply only to the top 12% of high-value homes – the vast majority of Canadians won’t pay a penny more. But it will help slow down home prices so earnings have a chance to catch up, demonstrating allegiance to the Canadian dream that a good home should be in reach for what hard work can earn.

Reduce collateral damage from the cheap credit system

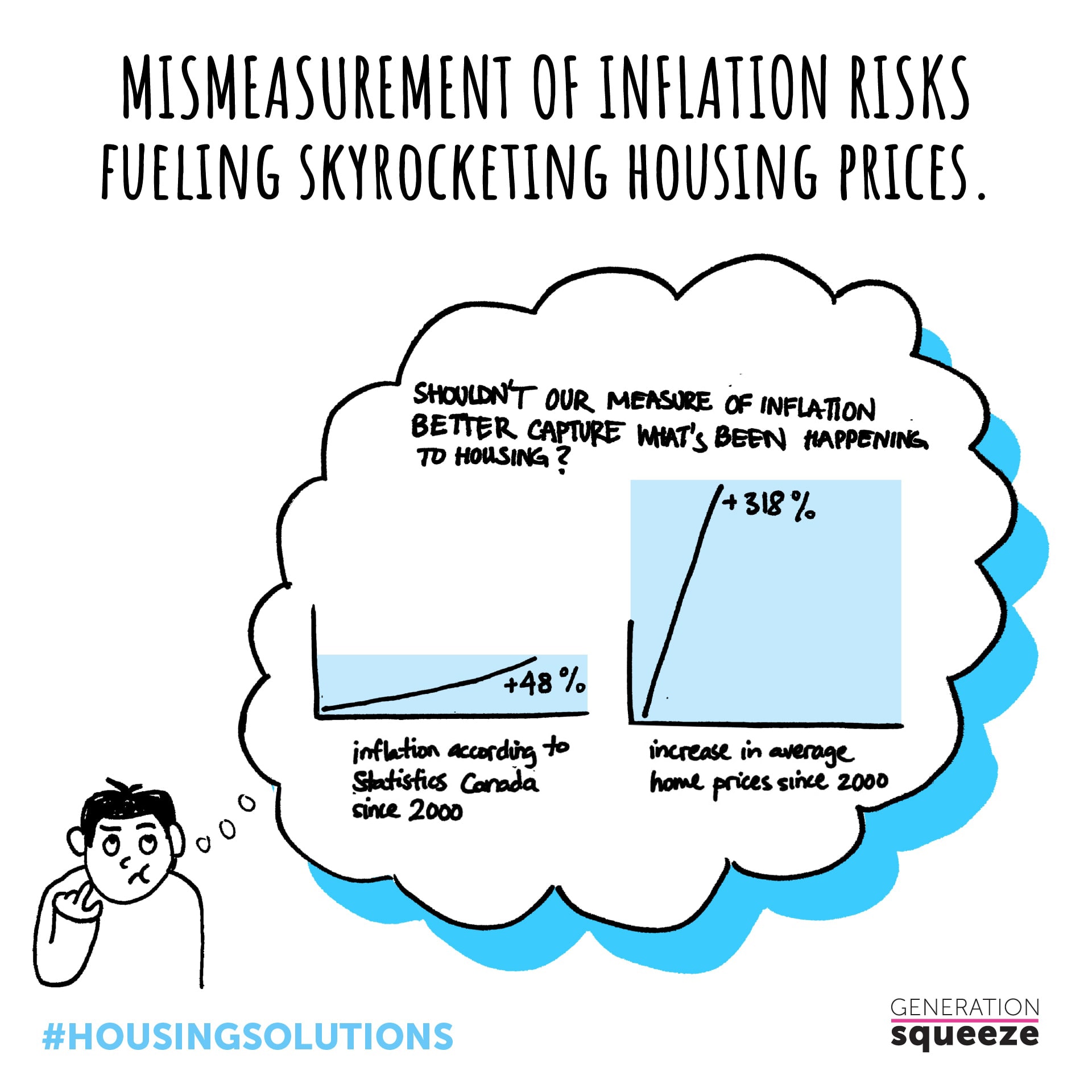

Since 2000, average home prices have risen by a whopping 318%. Yet over the same period, Statistics Canada reported that total inflation rose by 48%. That’s a pretty major disconnect.

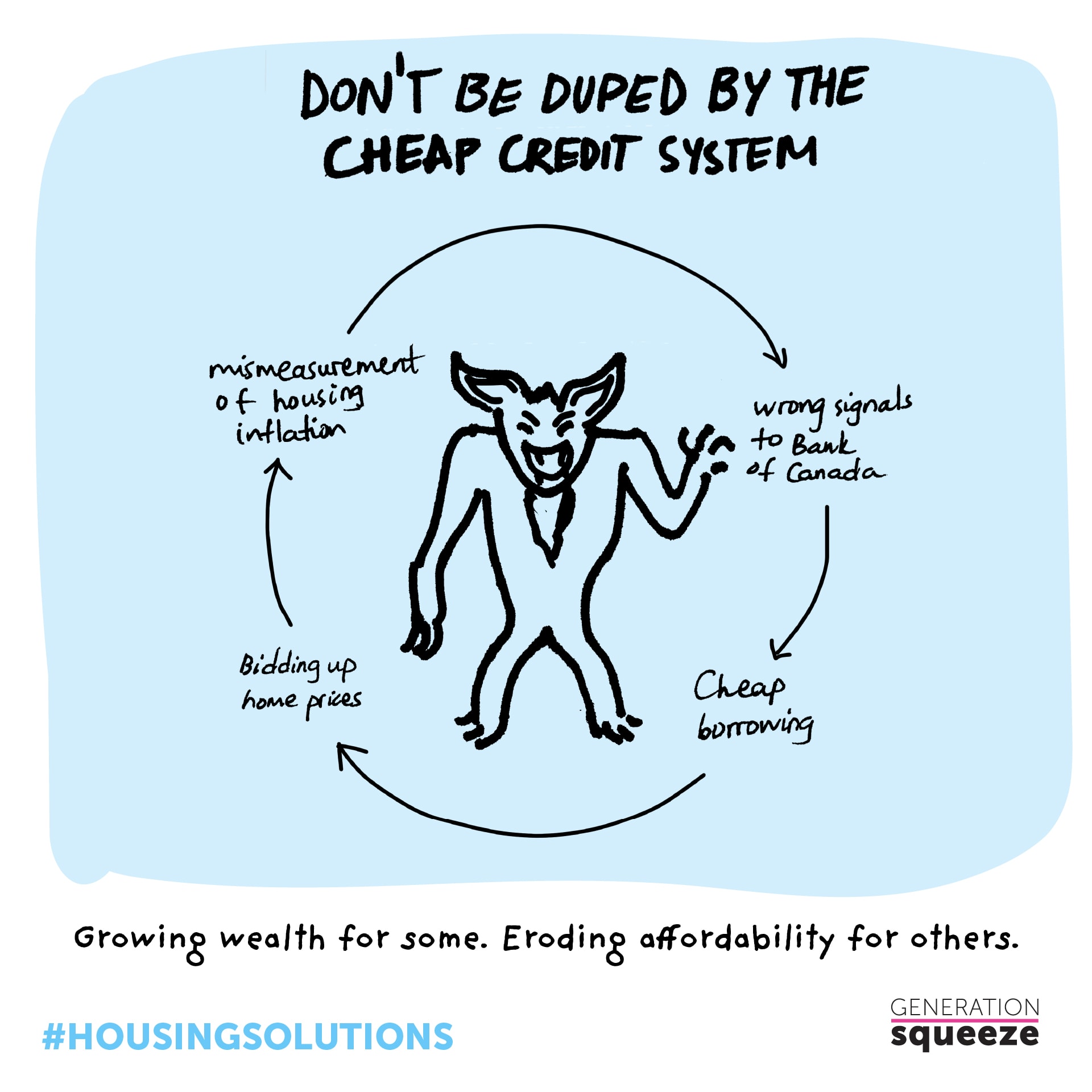

Gen Squeeze is calling on Statistics Canada to remedy its flawed inflation measure, which prioritizes the experience of existing homeowners and underestimates challenges facing those hoping to buy homes for the first time. This measure sends wrong signals sent to the Bank of Canada, causing it to overlook housing prices when setting inflation policy. That’s why recent increases in food and gas prices have triggered interest rate hikes – while decades of increases in home prices did not.

Underestimating inflation betrays younger Canadians by sustaining the cheap credit system. Low interest rates decrease the cost of larger mortgage debt. Buyers able to borrow more bid up home prices. Rising prices aren’t adequately captured in inflation data – creating a feedback loop that helps fuel prices beyond earnings.

Yes, some first-time buyers want the lowest possible interest on frighteningly large mortgages they must borrow to straddle the massive gap between home prices and earnings. But this individual coping strategy reinforces larger trends that work against first-time buyers, because they aren’t the only ones borrowing. Current homeowners with more capital use low interest rates to outbid their novice rivals. That’s why Census 2021 data reveals that more new homes are bought by investors, and then rented out to younger people; and that one in six Canadian homeowners now owns multiple properties.

{kind=link}

{kind=link}

{kind=link}

{kind=link}