Scale up Non-Market Housing

Non-market housing is housing protected from market forces, meaning more affordable rents and prices over the long-term. It makes up a small fraction of Canadian homes, much of it built...

Big thanks to the Balanced Supply of Housing Community-University collaboration for helping to co-create this strategic framework and the visualization.

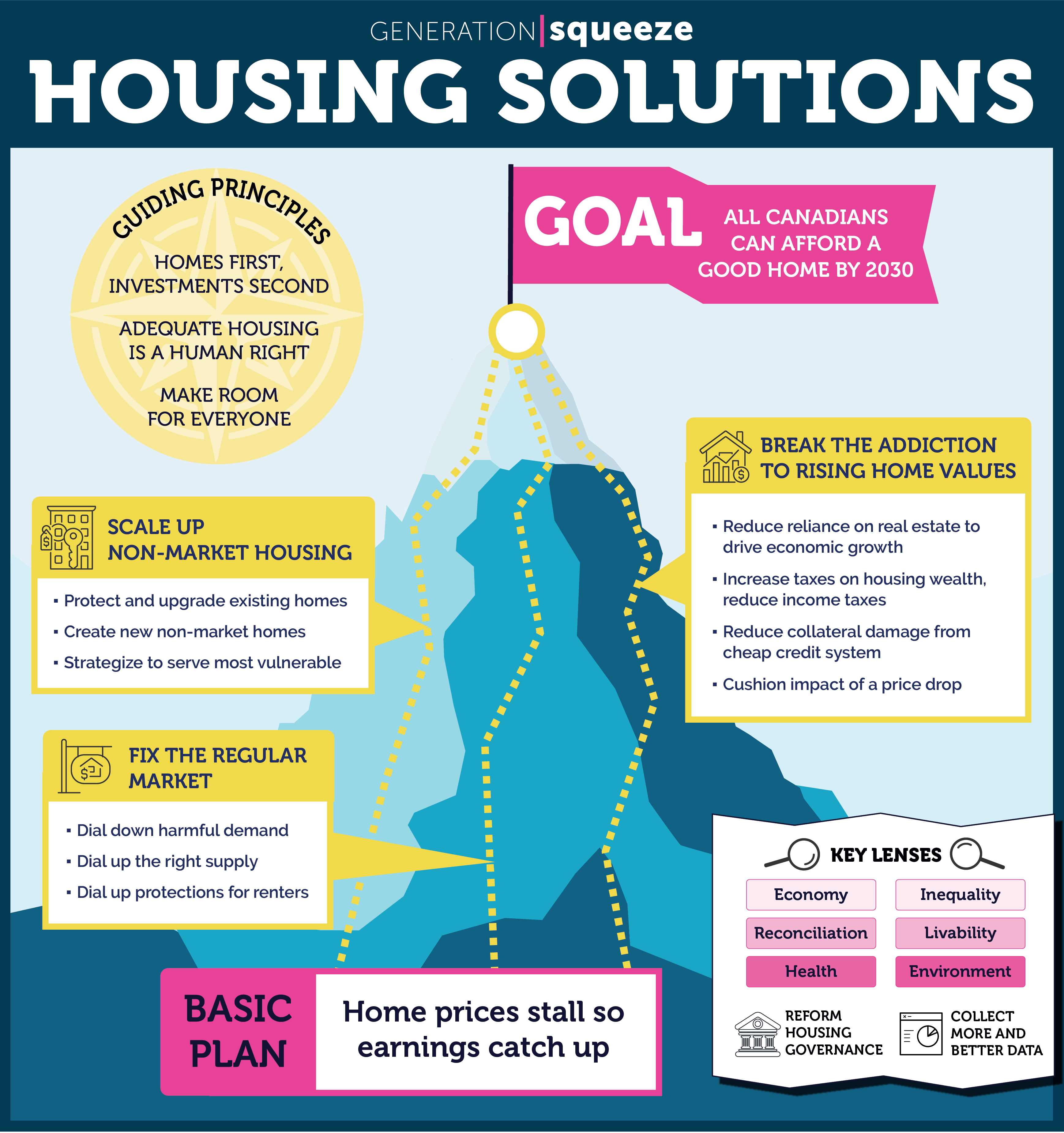

To solve any complex problem you have to get the first principles right. If you don't, the system will continue to lean in the direction of the problem, no matter how hard you try to fix individual pieces. Here are three principles we think are necessary to fix the complex problem of housing unaffordability:

The concept that all people have rights to which they are inherently entitled simply because they are a human being allows us to defend against the worst tendencies of our political, social and economic systems.

One of the basic human rights is the right to adequate housing and shelter, recognized in the Universal Declaration of Human Rights, the International Covenant on Economic, Social and Cultural Rights, and in Canada’s own legislated National Housing Strategy.

This right will have different meanings in different contexts, such that its definition and achievement is an ongoing process. Fundamentally, it means that if we’re capable of offering access to adequate housing and shelter to everyone in Canada, then we do. It also requires us to address the many kinds of discrimination that exist in our housing system, and to include marginalized voices in decision-making.

To realize this right, we need to pick other first principles that lean the entire housing system towards its achievement. And that’s where the next two principles come in.

One of the root causes of housing unaffordability is the so-called “financialization” or “commodification” of housing.

Making money on housing by building or improving it, or by operating well-maintained rental suites at fair rents is normally a good thing, because it helps people secure a home.

Things become overly “commodified” when the mere ownership of homes and land is treated as an investment strategy — with the aim being to gain wealth (beyond principal payments) without really doing anything at all.

This kind of commodification (a.k.a. speculation) leads to institutional and individual expectations or dependencies on a type of profit that often comes at the direct expense of others’ ability to find and afford a good home.

This guiding principle calls us to treat housing more as a place to call home, and less as a way to get rich, and can be applied to every category of action in this solution framework.

This means all housing policy should be created with the intent of welcoming a diversity of people, incomes, quality housing forms, and tenures into all of our neighbourhoods and communities.

It is a response to existing housing policies (e.g. zoning regimes), practices and attitudes that drive urban sprawl and intentionally or unintentionally, partially or wholly, and proactively or reactively have the effect of excluding groups of people (inc. renters, people of colour, low and middle income people, immigrants, and families) from living in quality housing near desired jobs, amenities and family.

This guiding principle can be applied to every category of action in this framework. In some cases the application is direct (e.g. dialing up supply) and in other cases indirect (e.g. any action that lowers costs can have the effect of making room).

Home prices stall so earnings catch up

Affordability can be restored through some combination of higher incomes and lower costs. In many Canadian communities, housing costs have risen so sharply that it’s unrealistic to expect many peoples’ incomes to catch up.

So, while this plan includes opportunities for direct and indirect income support (e.g. renters’ benefits, lower income taxes), its major focus is on reining in housing costs.*

A major area of debate is whether non-market housing, rental housing, and hybrid-tenure housing (e.g. fractional ownership) can realistically and sustainably ensure affordability for all even in a context of stratospheric home and land values.

This basic plan assumes that they cannot (or that it would be extremely difficult), and that some decline in home and land values is required to achieve and sustain the goal.

*We also need to rein in other costs such as child care, parental leave and transportation costs, which themselves can add up to mortgage or rent-sized payments.

In addition to this three-pillar plan, there are two more requirements to ensure affordability.

To ensure that everyone in Canada can afford a home that meets their needs. Indigenous, federal, provincial, territorial, and municipal governments need to work together.

Intergovernmental collaboration can be difficult at the best of times, and the governments who are closest to the housing issue (local and indigenous governments) often have the least resources and authority to address it.

Many would say the value of housing investments by federal, provincial and territorial governments is still inadequate, often with too much red tape in the way of accessing it.

One way to reform housing governance would be to increase the amount of provincial and especially federal funds dedicated to the issue. Another way would be to rethink the current division of powers such that local and indigenous governments have more direct authority and resources to achieve the goal in locally-tailored ways.

While there are ongoing efforts to improve the amount of housing data collected, synthesized and shared between governments and the public, some feel there are still too many gatekeepers, and large data gaps, making it difficult to make evidence-based decisions.

Additional efforts should include a federal beneficial ownership registry, robust information on global capital flows into Canadian residential real estate, robust data about the influence of monetary policy, the mortgage market and lending on rising home prices, better information on evictions, housing discrimination and equity, secondary rental market, rigorous assessments of local housing needs, and more.

All housing policy should be viewed through a reconciliation lens.

That is:

All housing policy should be viewed through an economic lens.

That is:

This lens immediately triggers different views on what is or isn’t healthy economic activity when it comes to housing.

For example, this framework’s second guiding principle of “Homes First, Investments Second”, the “Basic Plan” that focuses on reining in costs, and the third policy pillar of “Break the addiction to high home values” contains an embedded critique of Canada’s current degree of economic reliance on rising home and land values.

Housing should be central to any government’s economic strategy. Rather than focus on spurring ever- higher values, the focus should be on the productivity gains and the avoided social costs created by ensuring everyone has an affordable home that meets their needs. It is time to imagine an economy that is stimulated by a housing system which reconnects the cost of living to local earnings in order to support employment and growth in other industries.

This is especially true as Canada seeks to recover from the Covid-19 pandemic, which has disproportionately impacted those least likely to have stable housing at the outset.

All housing policy should be viewed through an inequality lens.

That is:

All housing policy should be viewed through a health lens.

That is:

All housing policy should be viewed through a livability lens.

That is:

All housing policy should be viewed through an environmental lens.

That is:

This strategic framework was co-created with the Balanced Supply of Housing (BSH) Community-University collaboration.

The starting place was a policy framework originally developed by Eric Swanson (now of Third Space Planning), during his tenure as ED for Generation Squeeze. The initial framework was itself based on several years of housing research, advocacy, and multi-stakeholder dialogues led at Generation Squeeze. This starting framework combined a simple summary diagram with explanatory text.

Through a series of twenty in-depth interviews conducted in 2020 with members and partners in the BSH collaboration, Eric and the Gen Squeeze team gathered feedback and insights that were used to improve and upgrade the starting framework.

The idea was not to create a perfect framework that enjoys 100% consensus, but to develop an increasingly strong “living” product that does a reasonable job of uniting different perspectives and areas of focus. The intention is to make regular improvements to the framework over time, incorporating more and more perspectives, and new information. It is anticipated the policy framework will be revisited annually

as part of the collaboration's team-building activities, and as a strategy to synthesize findings from the various research projects funded by the collaboration.