Ottawa's Spring Economic Statement: Another missed opportunity?

Ottawa prioritizes $17 billion for retirees with six-figure incomes over transformative affordability measures

Ottawa prioritizes $17-billion for retirees with six-figure incomes over transformative affordability measures

Fiscal updates are meant to show how governments will use scarce dollars to meet the moment. This week’s spring economic statement shows something else.

The Carney government missed another opportunity to deliver the biggest improvements to affordability and income security in decades — without raising tax rates or the deficit.

Consider what was left on the table:

- Canada could have eliminated seniors’ poverty by adding $5,000 for each of the 400,000 older Canadians below the poverty line.

- We could have delivered a $3,000 annual rent subsidy to a million young people struggling to afford a place to live.

- We could have maintained the full $4,200 Canada Student Grant for a million postsecondary students, instead of cutting it to $3,000.

- We could have subsidized 100,000 more $10-a-day child care spaces, meeting Ottawa’s target of 250,000.

- We could have expanded the Youth Climate Corps from a 1,000-person pilot to tens of thousands — helping young people build skills, earn a living wage, strengthen climate resilience, and reduce unemployment.

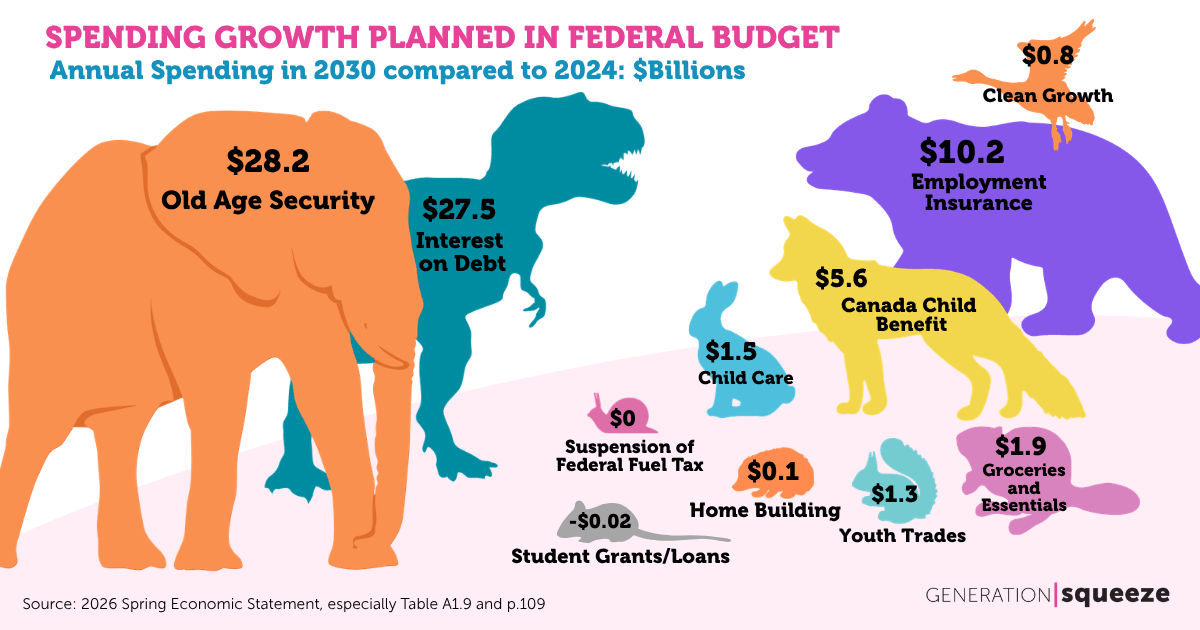

All of this could have been paid by modernizing Canada’s largest income subsidy, Old Age Security.

According to the latest figures, OAS cost $80.3 billion in 2024/25 and is projected to reach $108.5 billion by 2030/31. It absorbs more new public spending than any other federal program.

About 16% of OAS spending goes to retirees with household incomes above $100,000 — often delivering benefits to couples that exceed $18,000 per year.

By 2030, that share alone will total roughly $17.5 billion annually flowing to retirees with six-figure incomes.

That number is more than double what Ottawa spends on $10-a-day child care. It is nearly ten times larger than this spring’s investments to make it easier to afford a home. It dwarfs all spending announced in the spring statement for groceries supports, trades training and clean growth – combined. It’s hundreds of times larger than the Youth Climate Corps.

And remember: this is just the portion of OAS going to financially secure retirees with six-figure incomes.

At a time when Ottawa projects deficits above $50-billion annually for years to come, it is essential to ask: is this really the best use of public dollars?

Especially when the alternative is so straightforward.

It’s time to trim OAS benefits by about $3,000 after tax for retirees with household incomes above $100,000. This change would protect or improve benefits for roughly 80% of seniors, while reducing subsidies for the top 20% of OAS recipients.

This alternative would not cut OAS spending. It would simply slow its growth: projected spending would be closer to $100-billion instead of $108.5-billion by the end of the decade.

The roughly $9-billion in annual savings would be drawn entirely from retired households whose incomes are 35% above the national median.

That is enough to do everything listed above: eliminate seniors’ poverty, strengthen student supports, expand child care, help young renters and invest in youth employment to make Canada more climate resilient — all at once.

Canadians are ready for this change. Polling consistently shows that about three-quarters support modernizing OAS in this way, including three-quarters of seniors.

The case becomes even clearer when compared with Ottawa’s broader fiscal efforts.

The federal government is working hard to generate about $12-billion in annual savings through its comprehensive expenditure review. But one well-designed reform to OAS could deliver nearly as much on its own.

At a time when we face domestic affordability pressures, geopolitical uncertainty and rising risks from extreme weather, we cannot afford to overlook changes that deliver this scale of impact. We should double our ambition by pairing a careful spending review with targeted OAS reforms that unlock major gains.

I’m not suggesting that a six-figure household income in retirement makes someone “rich,” and I know some would prefer to make fiscal room by taxing fortunes above $10 million. But even if adopted, that approach would not solve Canada’s fiscal or affordability challenges. The NDP proposed such a move in the last election, and it would raise about $23 billion a year. That’s less than half the current deficit, and less than the projected growth in OAS spending over the next five years.

If the goal is to build a stronger Canada in which all seniors live in dignity and younger generations can afford to build a good life, then modernizing OAS is the clearest place to start.

Until that happens, we will keep tying one fiscal hand behind our back — leaving transformative improvements to affordability within reach, but out of grasp.